Source: Google Street View, 3636 North Broadway, Chicago IL

Last Thursday, Walmart ended its Walmart Express concept, shuttering all 102 such stores. Walmart announced earlier in January that they planned to close several underperforming stores across all of their formats, but it was the entirety of Walmart Express that made up the bulk of the planned closures. Despite that fact, the Walmart Express format meets a relatively quiet end, as discussion of Walmart store closures as an economic indicator largely drowned out discussion of the Express format itself. It is a format that deserves some further examination.

Launched in 2011 with great expectations, Walmart Express stores were between 12,000 and 16,000 square feet. While carrying a variety of general merchandise, they were decidedly grocery-focused, with a product mix not unlike a Walmart Supercenter. Many included a pharmacy, a gas station, or both. The format was positioned directly at small-format discounters such as Dollar General and Family Dollar, as well as single-price dollar store chains like 99¢ Only and Dollar Tree. While certainly intended to compete with these stores in rural communities too small to support one of Walmart’s larger stores, the format’s greatest promise was to be its ability to get Walmart into dense, pedestrian-heavy, urban neighborhoods. Walmart has long struggled to penetrate dense urban areas, at least in part because of the difficulty of finding locations with enough land to support one of their existing formats. With its small size and the success of the aforementioned competitors in urban markets, Walmart Express appeared poised to finally bring Walmart downtown. Some even thought it could be a powerful new weapon in the war against urban food deserts. Two of the earliest Walmart Express locations were in urban Chicago, one roughly a mile from the Navy Pier and the other just blocks away from Wrigley Field.

Most of the stores were opened in states where Walmart is entrenched as the dominant retailer. Stores also opened in exotic locales such as Naples (Texas), Dover (Tennessee), Damascus (Arkansas), Prague (Oklahoma), and Italy (Texas).

Most of the stores were opened in states where Walmart is entrenched as the dominant retailer. Stores also opened in exotic locales such as Naples (Texas), Dover (Tennessee), Damascus (Arkansas), Prague (Oklahoma), and Italy (Texas).

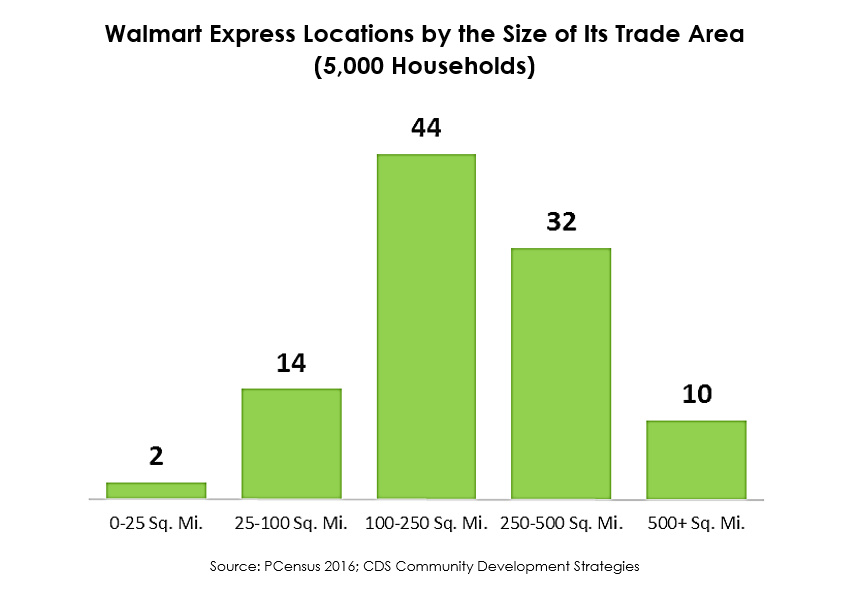

Of the 102 Walmart Express stores that ultimately opened, only the two Chicago stores were in anything that could be considered close to urban. The remaining store locations were not only rural, but rather sparsely populated. This is understandable as Walmart is already present in other more ideal markets with their standard and supercenter formats. The following chart depicts just how rural the markets were that contained a Walmart Express. Each store has been put into a category based on how large a radius would be needed to contain 5,000 households.

As demonstrated by the data, most of the Walmart Express locations are in very rural markets. The majority of stores required over 100 square miles to serve the nearest 5,000 households. For a handful of stores, this area was over 1,000 square miles. The two locations that required less than 25 square miles are in Chicago; both required less than 1 square mile to find 5,000 households. It has been argued that the rural Walmart Express locations were poorly merchandised and were too close to existing Walmart locations (“close” being a relative term in communities where driving many miles to Walmart for a weekly shopping trip is quite common). There is some truth to both of these points, especially for the Chicago stores, but after looking at the data it appears the biggest challenge for the Walmart Express may have been the site selection.

That Walmart stuck with the Express concept for so long is not surprising. It takes time to evaluate a new retail concept and Walmart has a precedent for patience. From 2009 to 2014 they conducted test runs for a pair of Latino-focused concepts, Mas Club and Supermercado De Walmart; both now extinct. What is surprising about the Walmart Express experiment is its size. While a drop in the bucket compared to Walmart’s entire portfolio, 102 stores seems more than just an experiment. In contrast, just a single Mas Club and only two Supermercado De Walmart stores were ever opened. The two Walmart Express stores in Chicago do seem comparable to these earlier experiments, and it is clear Walmart was disappointed with their performance early on as they did not expand the format further in urban markets. The decision to open 100 other locations, all in sparsely populated areas, remains puzzling.

That Walmart stuck with the Express concept for so long is not surprising. It takes time to evaluate a new retail concept and Walmart has a precedent for patience. From 2009 to 2014 they conducted test runs for a pair of Latino-focused concepts, Mas Club and Supermercado De Walmart; both now extinct. What is surprising about the Walmart Express experiment is its size. While a drop in the bucket compared to Walmart’s entire portfolio, 102 stores seems more than just an experiment. In contrast, just a single Mas Club and only two Supermercado De Walmart stores were ever opened. The two Walmart Express stores in Chicago do seem comparable to these earlier experiments, and it is clear Walmart was disappointed with their performance early on as they did not expand the format further in urban markets. The decision to open 100 other locations, all in sparsely populated areas, remains puzzling.

Walmart Express next to Dollar General in Richfield, North Carolina, population 614

The failure of Walmart Express seems unlikely to generate much fallout. The company is not unhealthy and is still expected to open more new stores in 2016 than they will close. Nevertheless, Walmart Express’ inability to crack dense urban markets or successfully respond to the dollar store chains will hamper Walmart’s long-term growth prospects. The greatest effects will be felt in the 100 small towns that now find themselves with an empty retail building.

About the Author: Ty Jacobsen is a GIS and Market Analyst with CDS Community Development Strategies. He specializes in demographic research and analysis, and has long held an interest in grocery retail due to his father's 30+ years of work in the industry.

RSS Feed

RSS Feed